CREDIT UNIONS

Why credit unions are a perfect fit for BIP

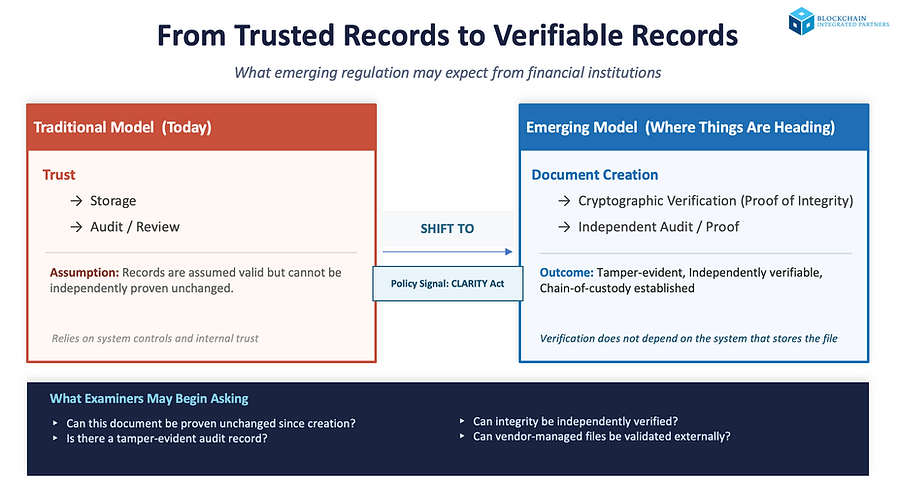

Credit Unions are facing rising regulatory pressure around document integrity, auditability, and digital asset workflows. The 2025 CLARITY Act, alongside the GENIUS Act, is a clear signal that regulators are moving toward proof-based recordkeeping, where institutions must demonstrate that critical files have not been altered. This pressure is expected to center on digital asset handling, record integrity, auditable digital workflows, and chain-of-custody for member and operational data. Areas examiners will increasingly treat as examinable. BIP is uniquely positioned to become the compliance foundation Credit Unions need, delivering immutable audit trails and tamper-evident verification without disrupting existing systems. BIP enables proof-based compliance through independent, non-repudiable verification, giving Credit Unions affirmative evidence that records remain authentic from creation through every handoff.

Credit Unions manage highly sensitive member and operational records, including loan and collateral documents, title files, internal compliance materials, and board reporting. Unlike traditional systems, BIP creates a verifiable chain-of-custody for these records, exactly the kind of capability federal examiners are beginning to expect. Credit Unions are also market-efficient for BIP because they rely heavily on Credit Union Leagues and Associations to vet and recommend trusted technology. One strategic league relationship can translate into dozens, even hundreds, of Credit Union opportunities.

The market pathway through credit union leagues

Leagues function as franchised buyer networks with existing trust. For example, one credit union league represents roughly 300+ Credit Unions and provides direct access to compliance offices, CIO/CTOs, conferences, workshops, and government relations channels. BIP is positioned as a league strategic partner. We have immediate credibility, potential speaking slots, webinars, and repeatable licensing opportunities across an entire region.

The CLARITY act of 2025: a regulatory tailwind

The CLARITY Act (H.R. 3633) is the most significant federal legislation to date addressing digital assets, blockchain technology, and financial-sector data integrity. It passed the U.S. House in September 2025 and is now currently under review by the Senate Banking, Housing, and Urban Affairs Committee. Even before final enactment, it signals where oversight is heading, especially for Credit Unions.

Key CLARITY-driven expectations Credit Unions should prepare for include:

-

Traceable, verifiable, tamper-evident digital asset records

-

Blockchain-enabled verification frameworks for authenticity and data lineage

-

Time-stamped, immutable logs and demonstrable chains-of-custody

-

A shift from “trust-based” to proof-based compliance evidence

These expectations extend beyond digital-asset activity into the records that support member transactions, lending and collateral workflows, internal controls, and third-party/vendor data exchanges. This creates a powerful regulatory “pull." Credit Unions won’t be choosing compliance tooling as “nice-to-have”, they’ll need it to remain exam-ready.

Click here to read more on the Clarity Act:

The compliance gap Credit Unions can’t currently provide

Most Credit Unions rely on Loan Origination Systems, enterprise document management, shared drives, cloud storage, and internal databases. These systems do not provide independent proof of:

-

whether a file was altered

-

who altered it

-

when it changed

-

whether a third party modified it

-

whether a copy is identical to the original

This gap is exactly what CLARITY and GENIUS Acts are poised to make examinable.

What regulators are likely to ask next

As legislative direction becomes examination practice, Credit Unions should expect questions like:

-

“Can you prove this document was never altered?”

-

“Can you demonstrate integrity since creation?”

-

“Do you have immutable, tamper-evident audit trails?”

Institutions without a clear answer may face findings, remediation plans, or heightened scrutiny.

How BIP supports CLARITY-driven compliance

BIP’s patented platform directly addresses emerging regulatory requirements by delivering:

-

Immutable record creation: cryptographic fingerprints committed to a secure private blockchain

-

Instant tamper detection: any change breaks the match to the original fingerprint

-

Audit-ready verification: irrefutable proof of origin, authenticity, and integrity

-

No workflow disruption: integrates alongside existing systems as a compliance layer

-

Exam-ready proof that no unseen edits occurred, allowing Credit Unions to demonstrate integrity continuously, not just at audit time.

Put simply: BIP turns Credit Union records into provable truth.

Strategic expansion beyond Credit Unions

The same government-aligned, regulation-driven commercialization pathway that opens Credit Unions also maps cleanly into other high-budget, high-compliance industries, including critical infrastructure, supply chain, healthcare records, and student data privacy. These sectors have the same immutable-data and audit-trail requirements that BIP patents solve.

Recommended actions for credit union leaders

Immediate (0–3 months)

-

Identify integrity-critical files (loan docs, audits, board materials, etc.)

-

Map current integrity and chain-of-custody gaps

-

Begin league-level education briefings (CrossState first)

Mid-term (3–12 months)

-

Implement immutable verification for compliance files

-

Extend tamper detection into member-facing workflows

-

Prepare internal audit for proof-based evidence standards

-

Establish vendor/third-party oversight specifically around data integrity and chain-of-custody expectations.

Long-term (12–24 months)

-

Move toward unified integrity frameworks across all critical documents

-

Align annual exam materials with CLARITY expectations